How Can You Stop Social Engineering Frauds Using Behavioural Biometrics?

Behavioural Biometrics Technology Is Redefining Modern Fraud Prevention Architecture

Behavioural biometrics technology is emerging as the most effective approach to real-time fraud detection in banking and fintech, especially as social engineering fraud, account takeover attacks, and money mule networks rise sharply in 2025. Traditional fraud detection software for banks relies on credentials, devices, and one-time authentication, but modern fraud succeeds after login, when users are manipulated into acting against their own interests.

This is why behavioural biometrics, intent-based security, and digital trust architecture are now central to AI fraud detection in banking (2025).

What Is Social Engineering Fraud?

Social Engineering Fraud Detection Starts With Understanding Human Manipulation Social engineering fraud is a form of cyber fraud that exploits human psychology rather than technical vulnerabilities. Instead of hacking systems, fraudsters manipulate users into sharing credentials, approving transactions, or bypassing controls themselves. This makes social engineering scams uniquely dangerous, because transactions appear fully legitimate to traditional security systems.

Common Social Engineering Fraud Methods in 2025

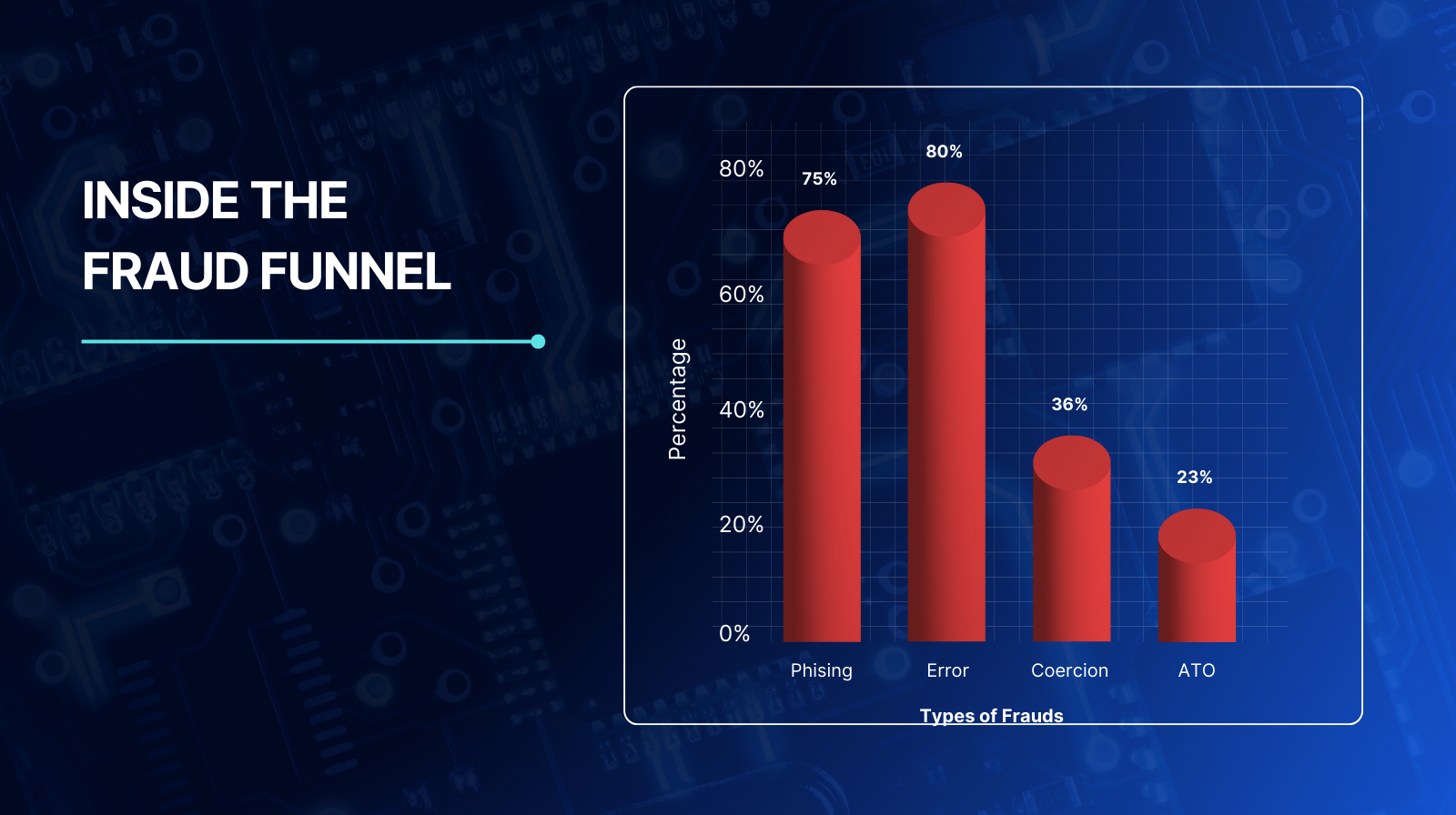

1. Phishing & Smishing Attacks Emails and SMS messages impersonate banks, fintech apps, or regulators to steal credentials or trigger fraudulent actions. Over 65% of social engineering attacks are phishing-based (2025).

2. Vishing (Voice Phishing) Fraudsters pose as bank officials, KYC agents, or police officers to pressure users into sharing OTPs or approving transactions in real time.

3. Impersonation Fraud Attackers impersonate executives, relationship managers, or government authorities to override skepticism and force compliance.

4. Investment & Loan Scams Fake returns, instant approvals, and urgency-based offers manipulate users into initiating transfers themselves.

5. Coercion & Duress Attacks Victims are pressured or threatened during live sessions, something credentials cannot detect.

Why Credentials Fail in Fraud Prevention

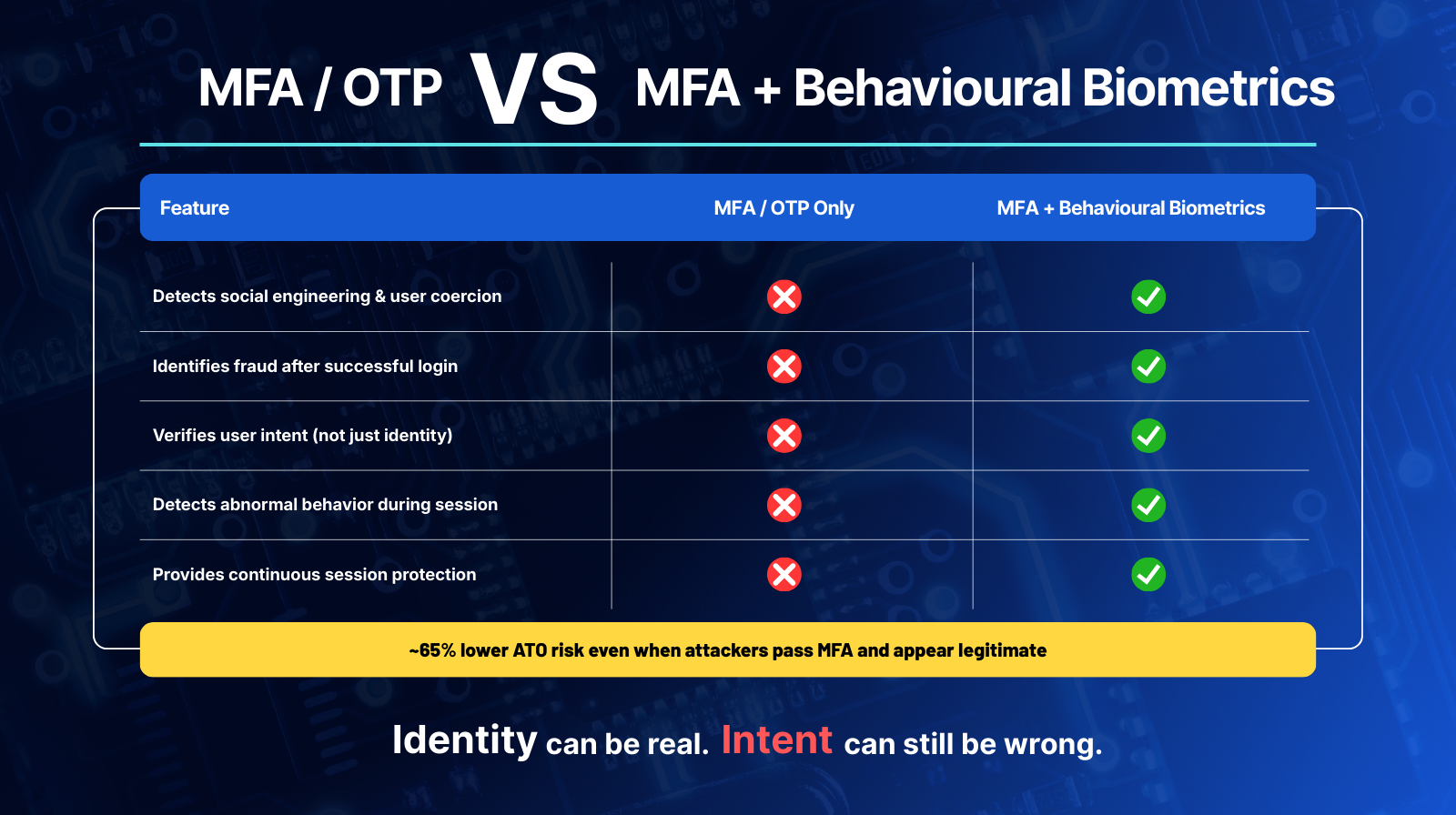

Why MFA, OTPs, and Passwords Don’t Stop Social Engineering

Most banks still rely on point-in-time identity verification. But modern fraud does not challenge identity — it exploits intent.

Key Reasons Credentials Fail:

- Credentials verify access, not intent

- MFA still passes when users are manipulated

- Account takeover attacks increasingly use valid credentials

- Systems cannot detect fear, hesitation, or coercion

- Fraud happens post-authentication

Most fraud in 2025 occurs after successful login. This is why modern fraud prevention architecture is shifting away from static controls.

What Is Behavioural Biometrics Technology?

How Behavioural Biometrics Detects Fraud Without User Friction

Behavioural biometrics analyzes how a user interacts with a device 'not what they know or have.

It continuously monitors:

- Typing rhythm

- Touch pressure and gestures

- Mouse movements

- Navigation flow

- Session behaviour patterns

Unlike MFA, it operates silently, continuously, and in real time.

The Key Shift in Digital Trust Architecture

From: Who are you?

To: Are you acting like yourself — right now?

This makes behavioural biometrics essential for:

- Fraud detection without user friction

- Detecting coercion in digital transactions

- Intent-based security in digital banking

How Behavioural Biometrics Stops Social Engineering Fraud in Real Time

Detecting Social Engineering Scams in Real Time Using Behavioural Signals

Behavioural biometrics flags subtle anomalies that indicate manipulation — even when credentials are valid.

Behavioural biometrics flags subtle anomalies that indicate manipulation — even when credentials are valid.

What It Detects:

- Sudden hesitation during payments

- Erratic typing after suspicious calls

- Unusual navigation paths

- Behavioural inconsistencies vs historical patterns

- Session-level anomalies across devices

How Banks Respond:

- Step-up authentication only when needed

- Transaction delays for high-risk actions

- Real-time alerts to fraud teams

- Silent user verification without friction

The Result: Fraud is stopped before money leaves the account — protecting customers, banks, and NBFCs from financial and reputational damage.

Behavioural Biometrics Use Cases in Fintech, Banks & NBFCs

Fraud Prevention for NBFCs and Fintech Platforms

- Prevent account takeover attacks in banking

- Detect money mule networks

- Stop social engineering-led fraud

- Enable AI fraud detection banking (2025)

Reduce false positives, Improve customer trust

Why Behavioural Biometrics Is Central to Fraud Prevention Trends 2025

Static security is now a liability.

Static security is now a liability.

.

Stop Protecting the Gate. Start Protecting the Session.

Cyber fraud prevention in 2025 is no longer about stopping hackers — it’s about protecting users from manipulation.

Cyber fraud prevention in 2025 is no longer about stopping hackers — it’s about protecting users from manipulation.

Behavioural biometrics technology delivers:

- Continuous trust

- Intent-based security

- Real-time fraud prevention

- Zero customer friction

If it’s not part of your digital trust architecture, you’re defending modern fraud with outdated tools

FAQ's

How does behavioural biometrics detect fraud?

Behavioural biometrics detects fraud by continuously analyzing user interaction patterns — such as typing, navigation, and touch behavior — to identify anomalies that indicate manipulation or unauthorized intent, even when credentials are valid.

How is behavioural biometrics different from traditional authentication in fraud detection?

Traditional authentication verifies identity at login, while behavioural biometrics continuously verifies intent throughout the session, enabling real-time detection of social engineering and coercion-based fraud.

Can banks detect fraud without MFA?

Yes. Behavioural biometrics enables fraud detection without MFA by silently monitoring behavior in real time, reducing user friction while improving security accuracy.

How do banks detect social engineering scams in real time?

Banks use behavioural biometrics and AI-driven risk models to detect hesitation, erratic behavior, and deviations from historical patterns during live sessions.

How does behavioural biometrics prevent account takeover attacks?

It detects behavioral inconsistencies during login and transactions, allowing banks to stop account takeover attacks even when valid credentials are used.

Can behavioural biometrics detect money mule networks?

Yes. It identifies abnormal transaction behaviors, session anomalies, and repeated deviations that signal mule activity across accounts.

Why is intent-based security important in digital banking?

Because modern fraud exploits human behavior, intent-based security allows banks to detect manipulation, coercion, and fraud that identity-based controls cannot see.

Is behavioural biometrics compliant with privacy regulations?

Yes. Behavioural biometrics analyzes interaction patterns, not personal data, making it privacy-safe and compliant with global regulations.

About The Author

Amit Chahal is the co-founder and Data Science head at Sign3, brings over a decade of experience in machine learning and financial fraud solutions, transforming how businesses safeguard against risks.