How Enterprises Can Defend Against Networked, Industrial-Scale Fraud in 2026

Fraud is no longer a series of isolated attacks. It is now an organized, technology-enabled economy operating at industrial scale. In 2025–2026, financial crime has crossed a structural threshold. Criminal groups now operate like distributed enterprises, using shared infrastructure, automation, and real-time coordination across accounts, devices, and platforms. For SMEs, fintechs, banks, and NBFCs, this changes the nature of defense entirely.

Static, transaction-centric controls were built for a different era. Today’s fraud economy is networked, behavioral, and adaptive and it is scaling faster than most risk frameworks.

The Scale Shift: Fraud Has Become a Systemic Risk

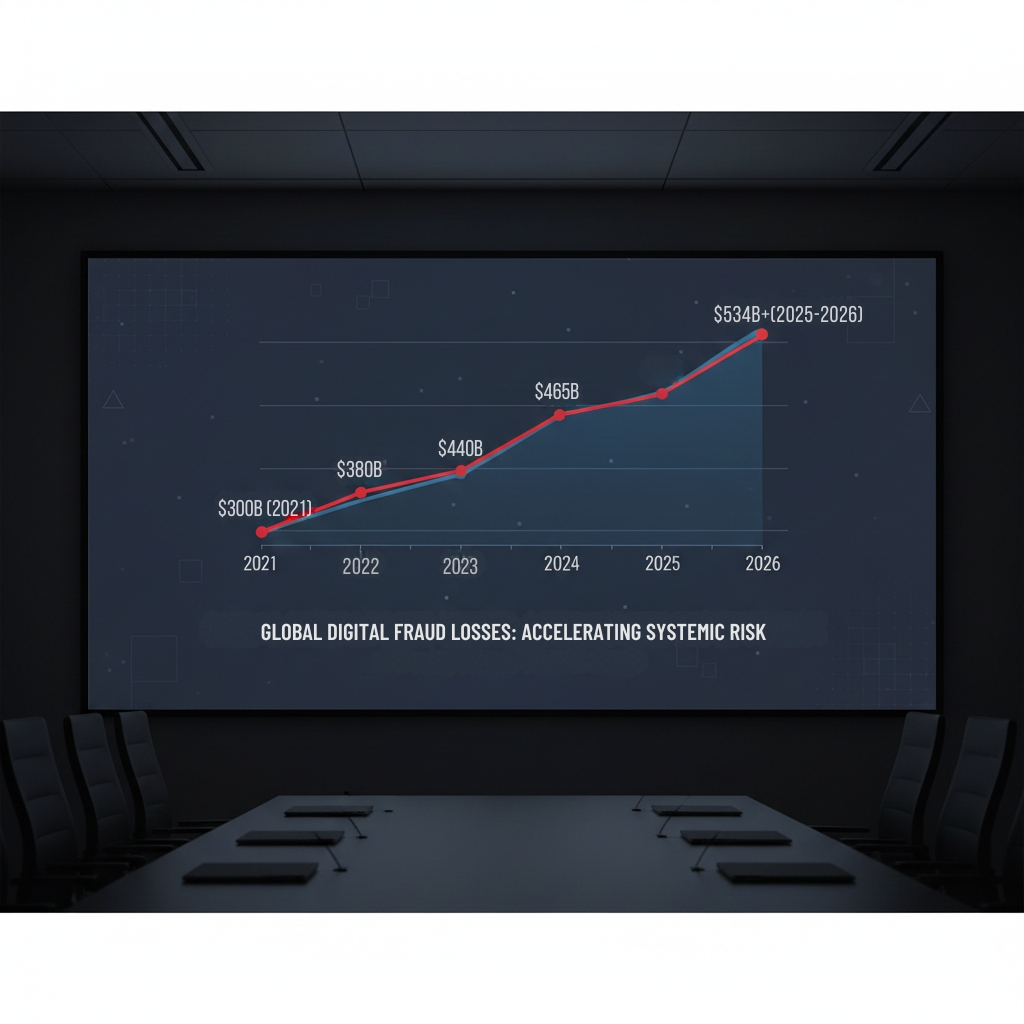

Recent intelligence confirms that fraud is no longer a marginal operational issue it is now a balance-sheet risk. According to TransUnion’s Global Fraud Report 2025, global digital fraud losses reached USD 534 billion, equivalent to 7.7% of average company revenue up from 6.5% the year prior. The Nilson Report (2025) estimates that global card and payment fraud losses exceeded USD 485 billion, reflecting sustained growth across digital channels. LexisNexis Risk and Experian estimate that over 55% of digital fraud losses are now linked to organized or repeat criminal networks, not one-off attackers.

Additional 2025–2026 signals:

- Business fraud losses increased 18% YoY globally (TransUnion)

- 24% of global losses now come from authorized push payment and scam fraud (TransUnion)

- 85% of organizations experienced deepfake-related fraud attempts in 2025, with average losses exceeding USD 280,000 per incident (IRONSCALES 2025)

- Global fraud rates have more than doubled since 2021, rising from 1.1% to 2.6% by 2024–2025 (industry meta-analysis)

- Over 70% of large fraud cases now involve multiple linked accounts and identities, indicating networked laundering activity (industry consensus from risk vendors)

Fraud has shifted from transactional to systemic.

Why Legacy Controls Are Structurally Outmatched

Most fraud systems were designed to answer a simple question:

Is this user legitimate at login?

Modern fraud answers a different question:

Can we manipulate a legitimate user after login?

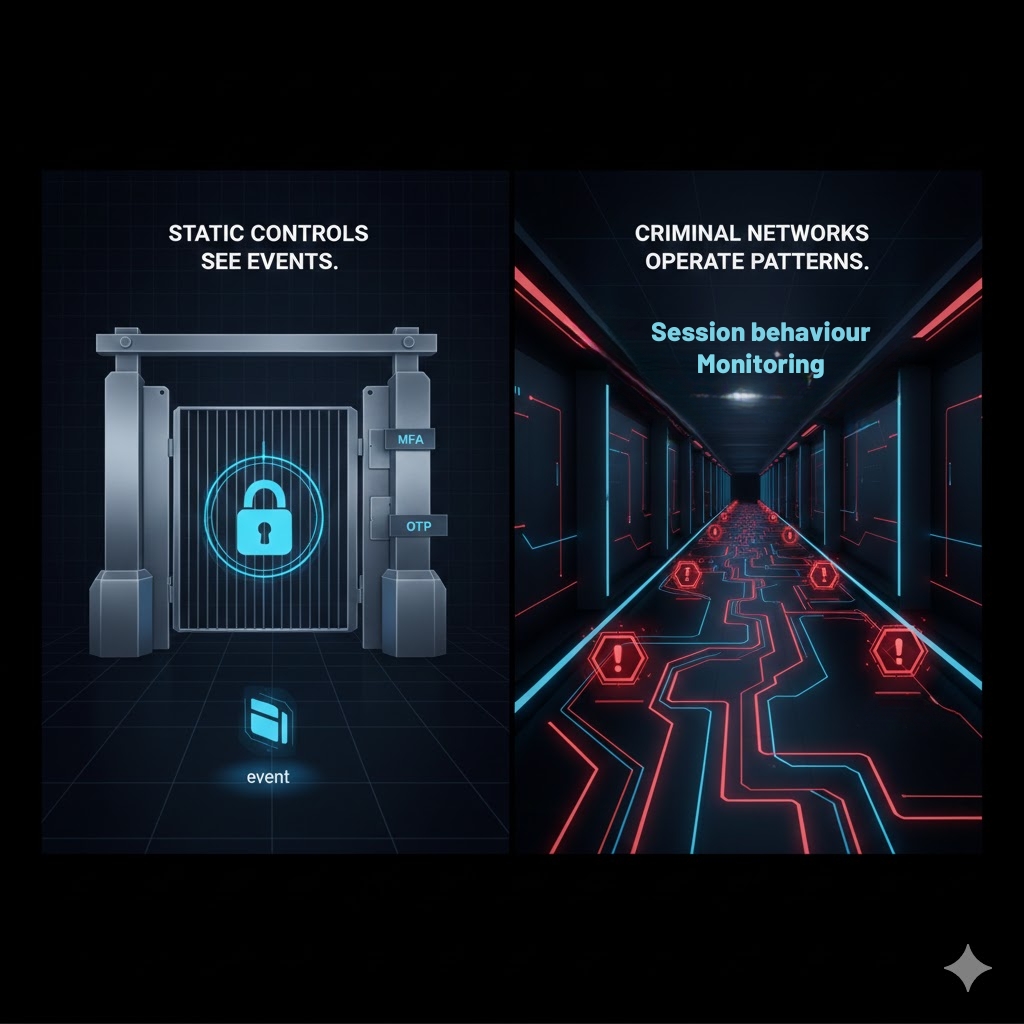

This is why credentials, OTPs, and MFA are no longer sufficient:

- Most fraud in 2025–2026 occurs after successful authentication

- Valid credentials are now a common input, not a security signal

- Social engineering and coercion bypass identity checks entirely

- Mule networks fragment activity across many low-risk transactions

Static controls see events. Criminal networks operate patterns.

The Rise of Networked, Industrial-Scale Fraud

Enterprises now face a new class of adversary:

Indian, Southeast Asian, and Eastern European fraud ecosystems increasingly operate with:

- AI-enabled impersonation and voice cloning

- Cross-bank mule and layering networks

- SIM- and device-based identity abuse

- Scripted scam operations at call-center scale

- Fraud-as-a-service platforms selling playbooks, tools, and access

These are not isolated attackers. They are coordinated, multi-layer systems optimized for speed and scale

Why Fintechs, Banks & NBFCs Are All Exposed

As digital finance accelerates, criminals exploit structural asymmetries:

- Faster payments vs slower detection

- Open onboarding vs fragmented identity signals

- Cross-platform movement vs siloed investigations

- Human manipulation vs system-centric controls

For SMEs and NBFCs, this often means losses surface only after funds are layered and dispersed.

For banks and fintechs, it means fraud increasingly becomes:

- A customer trust risk

- A regulatory exposure

- A reputational multiplier

- A balance-sheet threat

Fraud defense is no longer just about stopping transactions. It is about stopping networks.

What Modern Fraud Defense Requires

Defending against industrial-scale fraud requires a structural shift:

From isolated checks → to continuous intelligence

From account-level alerts → to network-level visibility

From static rules → to behavioral and intent-based detection

From post-event investigation → to in-session intervention

This is where modern fraud architecture changes the game

How Sign3 Helps Defend Against Networked Fraud

Sign3 is built for how modern fraud actually operates.

Across SMEs, fintechs, banks, and NBFCs, Sign3 enables:

- Behavioral biometrics to detect manipulation and coercion

- Device intelligence to identify repeat and coordinated actors

- Digital footprint analysis to surface hidden risk signals

- Network-level detection across identities, sessions, and behaviors

- Earlier intervention before funds exit the ecosystem

By focusing on session behavior, intent, and network patterns, Sign3 helps institutions move from reactive fraud response to proactive fraud disruption.

The Strategic Reality for 2026

-

You cannot stop an organized fraud economy with single checkpoints. Industrial fraud requires layered, continuous, and network-aware defense.

-

Fraud has become faster, more connected, and more automated than traditional risk frameworks were designed to handle.

-

The institutions that win in 2026 will be those that shift from protecting access to protecting behavior and from monitoring transactions to disrupting networks.

About The Author

Amit Chahal is the co-founder and Data Science head at Sign3, brings over a decade of experience in machine learning and financial fraud solutions, transforming how businesses safeguard against risks.